When I’m working with clients who have equity compensation there are three main areas of focus:

- The investment opportunity with the equity holdings

- The tax implication from the equity holdings

- Mitigating risks with the equity holdings

This last item tends to be the toughest discussion because most of these clients are passionate about their jobs and their companies and tend to look at decisions from a positive perspective of only more upside. In these discussions on risk, we look at various scenarios including the one where everything doesn’t work out as planned and the stock price declines. These discussions can vary widely depending on the type of company, the current stock price, market valuations, size of the holding, concentration risk, their station of life and their position in the company. Given the complexity of these benefits there tends to be a great deal of planning, and my goal is to provide a structured process that we agree to so that they find success regardless of the direction of the stock price.

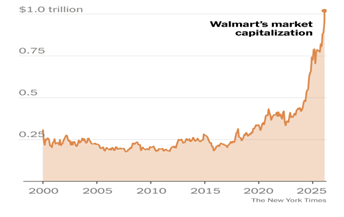

Two recent stock charts came to my attention last week that scream the need to have these planning discussions with executives in these companies. The first is Walmart (WMT). As the graph below shows, the stock has quadrupled in the past 6 years and increased 7 fold in the past 10 years. It’s price to earnings ratio is currently 44 and it’s historical PE is around 25. The last time it saw an increase this dramatic the stock plateaued for more than 10 years before moving higher. There are many reasons that Walmart’s stock price has increased dramatically and it has done an amazing job evolving as a company but for individuals who have equity comp in Walmart this is time for action. In these conversations I always remind investors that selling at these prices is as much about risk mitigation as it is a reflection of the future price of the company and as a general rule, I’m still expecting the stock price to move higher over time.

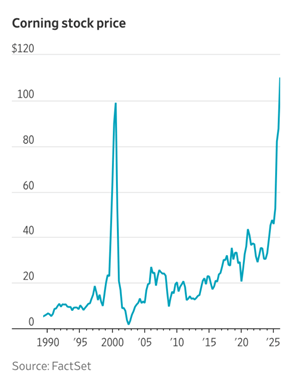

Another one that stood out to me is Corning (GLW) whose graph is shown below. Corning is doing extremely well, and the big driver behind its recent success is the glass fiber they manufacture which has been in huge demand with the building of all the AI data centers. This is another perfect example where the company is in a great position to do extremely well going forward but with the introduction of any new technology it is possible that demand for their fiber could continue at this level or it could drop very quickly. If there is any doubt how quickly things can change and impact the price of a stock all you have to do is look at the history of Corning stock. In the late 90s Corning saw substantial demand for their fiber as the demand for internet bandwidth increased and the bandwidth required building out fiber networks using Corning fiber (sound familiar). Things changed quickly after the tech bubble popped and the stock dropped dramatically not to hit a new high until this year!!

Again, it’s very important to stress that Corning’s stock could go higher which I hope it does for the employees of Corning, but it is possible that the stock could drop and having a disciplined plan in place that helps reduce an executive’s exposure to a company is extremely important from a risk mitigation perspective.

The other important item to consider in these discussions is not only the equity holdings and their connection to company but the compensation of the executive and their future career it also directly connected to the company. With these three areas combined, the importance or risk mitigation becomes that much more important.

Finally, when it comes to investing in a single stock there are many risks and opportunities with that company that can be identified if you are an executive but there are still many variables that are outside their control and even unknown to them. These are the risks that many executives don’t take into account when doing planning on their own and they can often be the most consequential.